Manager Analysis Services LLC (MAS), founded in 2003, provides customized services and expertise to benefit non-profits, Family Offices and Institutional Investors.

Professional governance services: MAS principals serve as Board directors for endowments, foundations, and nonprofit organizations. We serve on many boards, are experts at governance processes and fiduciary considerations, and bring the resources of our extensive network of financial industry and legal talents to the clients we serve.

Family office and trust-related services: We are experts for fiduciary matters for trusts and estates, and we serve as trustees and advisers for families. Unlike many trustees who specialize in one area such as law, investments, tax, or family experience, we have an exceptional capability to integrate all these considerations into a cohesive and comprehensive advisory approach. We can ensure that families’ investment strategies and service providers are appropriate and calibrated to the families’ needs.

Expert Portfolio Evaluations: MAS has performed 2,000+ investment manager evaluations, and each of our 3 principals has 25+ years of experience in investment management, risk, and portfolio analysis. We can assist with any client requesting help with specialized investment-related projects for any type of investment. Our credentials include JD, CFA and FRM designations.

MAS’s website has 20+ short policy papers posted on a variety of current Governance, Investment Management, Family Office, Portfolio Construction, ESG/Emerging Manager, and related topics so the reader may gain a sense of our range of expertise and focus. www.manageranalysis.com

Would a fresh look by expert practitioners help your Foundation or Family Office?

Please contact Chris Cutler, Tom Donahoe or Safia Mehta at 917 287 9551.

A family office came to Manager Analysis via a referral from a Family Office that we assist. The family leader had managed wealth carefully, and he benefited from the stock market’s long-term performance. However, because he had kept portfolio management considerations away from his children, and because the entire family wanted to plan for an orderly transition of responsibilities, the family asked Manager Analysis to review the family’s portfolios and identify any material threats to the assets.

The next generation was generally pleased with their current holdings, comprised primarily of liquid, larger cap equities, and muni bonds, and they did not want to alter the strategy. They also valued their operationally conservative profile and comparably simple legal structures. Virtually all of the assets were held directly and so the family was in a good position to control the timing of transactions to avoid unnecessary capital gains taxes.

Findings

The broker was attempting to gain discretionary control of the family’s portfolio through sleight of hand.

Buried within a simple “principal transactions agreement” was a commitment for the family to a second agreement, granting the broker full discretion. The family did not to sign the form because of our strongly delivered advice.

While portfolio turnover was low, the broker was charging commissions of 1% to 2% on large stock trades. He was seeking the opportunity to liquidate the entire estate’s liquid holdings to receive a $1 million commission. Comparable commissions would be about $125,000.

We also conducted reputational reference checks on the broker and found that he had been placing clients into the highest commission investment products permitted by his brokerage firm.

Resolution

We assisted the family in establishing accounts at other brokerage firms, who charge zero or near-zero commissions on equity trades, and we are currently in the process of moving their holdings.

Want to learn more? Please contact Chris Cutler, Tom Donahoe or Safia Mehta at 917 287 9551.

Endowments and Foundations continue to wrestle with determining the best way to manage their portfolios:

Build an in-house team?

Hire an Outsourced CIO team?

Or engage a Consultant Advisor?

Since most Endowments and Foundations (“E&F”) depend heavily on the success of their investment programs, solving this challenge is a key determinant of their ultimate success.

Our research goal was to observe how E&F offices are making this determination, based on their portfolio sizes and number of staff. We focused on the empirical data available for 35 Endowments and Foundations of various sizes. We used E&F’s that had the most verifiable information available in the public domain, reviewing their tax filings, public websites, and LinkedIn profiles to obtain the required information. The data is intended to answer the following four questions:

Key Questions Addressed

If you are planning in-house investment management, how do your staffing decisions compare with what others are doing currently?

What does an In-House Investment Office cost?

Is there a typical AUM transition point where E&F’s might transition between In-House or OCIO Investment team approach?

What are the specific staff roles and org chart characteristics for an In-House Investment Office?

What we learned was both expected and unexpected. Managing an “Endowment Style” Investment Office means managing a complex, private portfolio and a multitude of managers. Yet, the In-House Investment Office size appears to have a definite ceiling.

While the specific facts and circumstances of each E&F investment corpus and each non-profit’s internal structure or requirements are not publicly available, there is detailed information available on key aspects of E&F’s portfolio management. Specifically, we were able to obtain the actual headcounts and the total compensation of the most senior members of each investment team. This is not a scientific sampling, rather it is hard data from a cross section of AUM sizes from $50 mm to $12 Bn. Using this data, the reader will obtain additional perspective as they determine whether building internally or embracing the Outsourced CIO model is the best fit for their organization.

The information on each of the 35 organizations is arranged from largest AUM to smallest AUM. Here are our general observations.

Main Conclusions from the Research

In-House Investment Office

>$4Bn AUM generally have in-house investment staffs of 12-16 professionals.

$1 Bn to $2 Bn generally have in-house investment staffs of 4-6 professionals.

$500 mm to $1 Bn opt for either in-house management or Outsourced CIO.

$50 mm to $500 mm often have a single in-house professional or rely on an Investment Committee with/without assistance of a consultant. The sole in-house professional may be more of a liaison and may be focused more on development efforts. (Nearly half of this sized cohort have adopted the OCIO model per industry research.)

There appears to be a tug of war as to whether in-house or OCIO works best in the $750 mm to $1 Bn AUM range. We have seen non-profits grow past the $500 mm AUM and decide that they are large enough to build an in-house team. There have been some notable exceptions recently with some names just below the $1 Bn AUM level. Several have decided to scrap the in-house Investment Office model completely and embrace the OCIO model.

The total team compensation appears to be as follows, based on $AUM size:

Mega +$4 Bn AUM – $5 mm to $7.2 mm range

Large $2 Bn AUM – $2 mm to $3.5 mm range

Medium $1 Bn – $2 Bn AUM – $2 mm to $3 mm range

Small x<$500 mm AUM – $300 k-$400 k range

Our total compensation aggregate estimates rely on actual published total compensation numbers for typically the CIO and the next management level, e.g. Director of Public Markets, Director of Private Markets, MD’s, or Sr. Portfolio Managers. The compensation levels for analyst/operations level staff are estimated based on the specific titling/job description obtained. We omit all investment related costs, e.g. Bloomberg terminals, technology costs, office rent, custodial fees, due diligence travel/research, etc. since they vary widely depending on investment strategies. Moreover, the sum of all external investment consultants together can cost well over $1 mm p.a., especially for larger portfolios. Thus, these additional expenses are not immaterial.

Organization of the Remainder of the Briefing

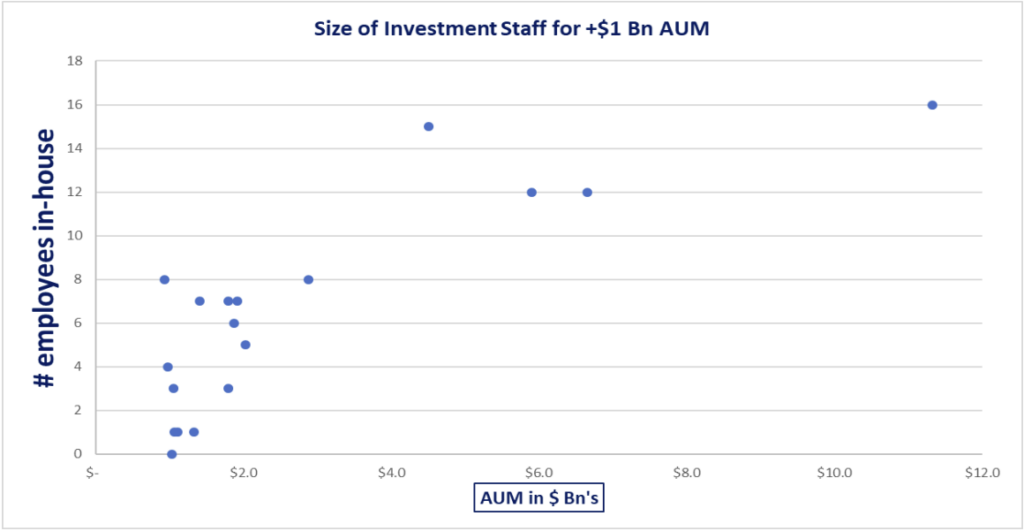

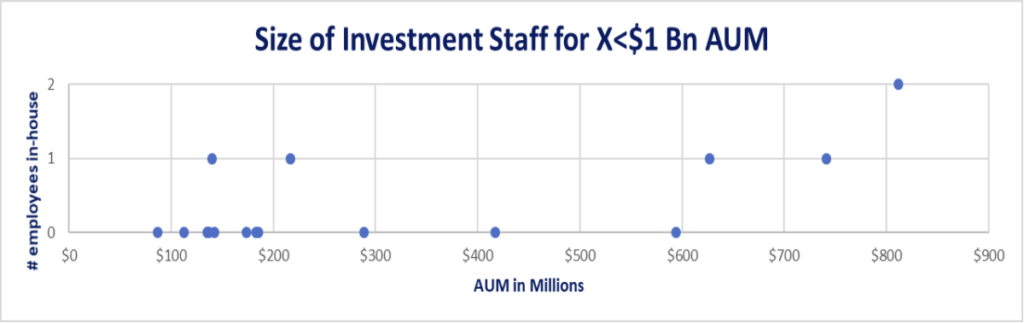

Two scatter plots present a comparison of in-house staff v. $AUM. +$1 Bn and X<$1 Bn)

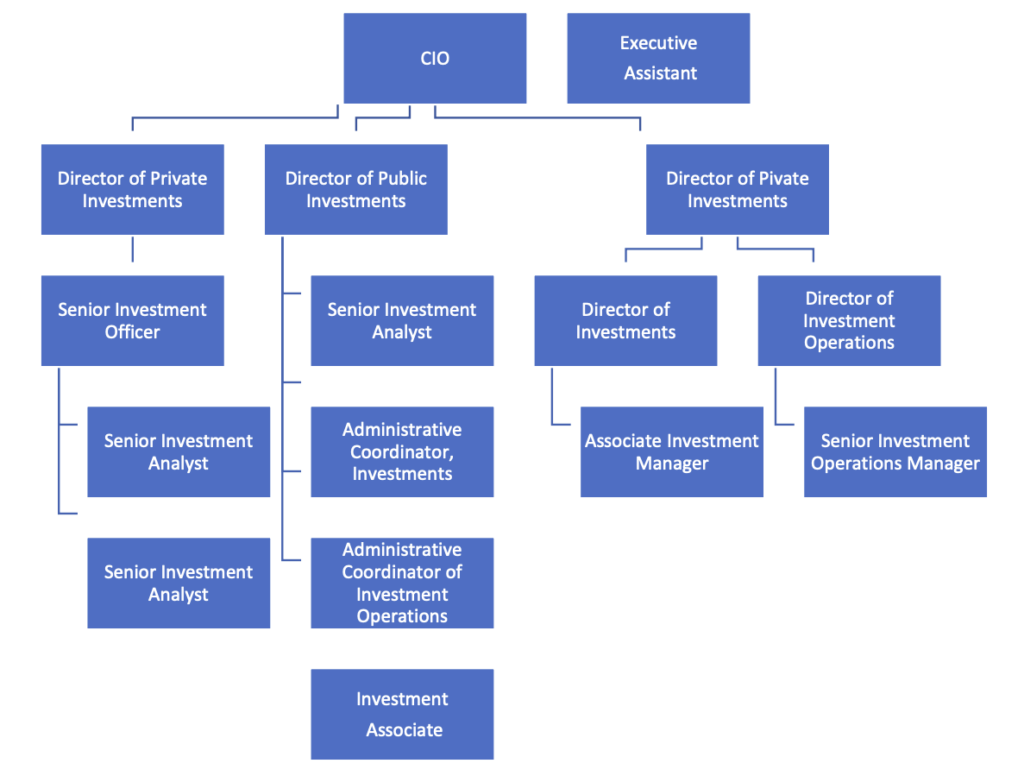

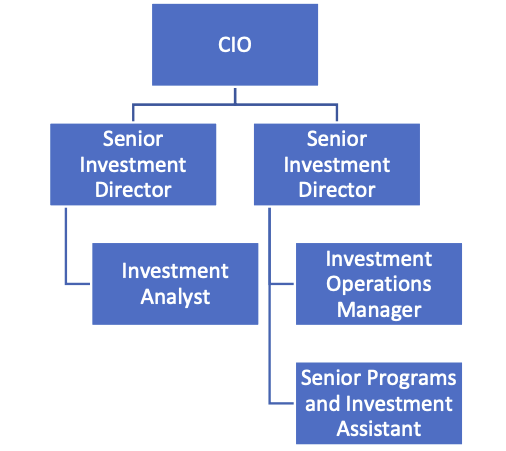

Organization Chart for a large >$10 Bn AUM team • Organization Chart for a $1 Bn to $2 Bn AUM team

Appendix that lists 10 large E&F’s and provides $ AUM, Staff size, positions by job titles, and total team compensation for the Investment Office.

Ratio of In-House Staffing Relative to Size of Endowment/Corpus

The scatterplot below for 18 Non-Profits demonstrates two staffing clusters. $4 Bn+ AUM leads to in-house staffing of 10 -16 investment professionals and support staff. $1 Bn to $4 Bn AUM leads often to in-house staffing of 4-8 Investment professionals. The staff figures are almost exclusively investment professionals but there are some admin or shared resources as well.

The scatterplot below for 17 Smaller Non-Profits demonstrates skeletal investment staffing: Less than $1 Bn AUM leads to in-house staffing of 0-2 investment professionals and support staff. Nearly half of the “0” in-house investment professionals reflects the adoption of either an OCIO or Consultant Advisory model. What is striking is that there are two E and F’s in the $650-$750 mm AUM range that are a one-person “team.”

Sample Org Chart for approx. $11 Bn AUM

Sample Org Chart for $1.5 – $2 Bn AUM

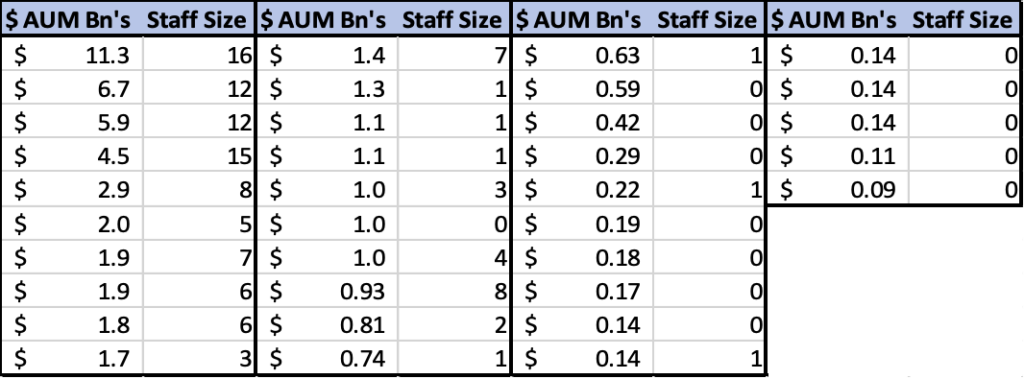

Summary Table of all 35 E + F’s by AUM and In-House Staff Size

APPENDIX

The goal of this appendix is to provide the reader with the staffing (by category) for 10 large Endowments or Foundations. The entities are ordered in descending $AUM size. All these E&F’s have built and maintained in-house Investment Offices. N.B. 2 entities (in the $750 mm – $1 Bn AUM range) opted recently to convert from in-house Investment Office to adopt the OCIO model. This range appears to be the inflection point where Boards/Committees struggle to decide what structure suits their organization best. The total compensation by team is included as well. Do note that under the Other category, it covers administrative roles that are not strictly investment-trained positions. Since they are included on the public websites of these E&F’s as being members of the “Investment Office”, we have opted to embrace this self-identification by the E&F’s.

Want to learn more? Please contact Chris Cutler, Tom Donahoe or Safia Mehta at 917 287 9551.

Many Family Offices place a premium on discretion and refrain from engaging expertise that does not emanate from a “close(d) circle” of advisers. The downside to this approach is that a Family Office exposes itself to the pernicious practice of being exploited, which occurs all too frequently across the wealth management industry. Families who are most comfortable with their “close(d) circle” of advisers are often the most exposed. Few cases are as severe as the Leslie Wexner case or the myriad losses from Madoff. The most frequent cases that we encounter involve excessive fees or efforts to misdirect trust proceeds.

The parties involved with these activities may not be the usual suspects. We have seen service providers play a material role in jeopardizing families’ legacies. Some examples include:

Health care providers for the elderly harassing elderly family members to change their wills and trusts—we have seen losses of 25% to 90% from these misdirections.

Trust and estate attorneys charging fees for settling large, yet simple estates as a percentage of assets rather than using a fair hourly rate, and poorly disclosing, if at all, that practice to families when they are facing tragedy from the death of a loved one.

Brokers charging commissions of up to 2% on equities trades when many firms charge little or no commissions for equities trades.

Collaboration or collusion among law firms, brokers, and accountants to maintain high fee schedules and discredit competing service providers in the eyes of family members. Conflicts of interest may be difficult to detect but can be devastating financially to families.

Private bankers charging all-in fees of 3% to 5% per year, when we believe a fair fee would be in the range of 1.5% per year. Since family offices are “sophisticated investors,” they do not have many of the legal protections of a retail investor. Family offices must work harder to uncover and understand “hidden” and poorly disclosed fees, long-term lockups, and other vulnerabilities in their investing process.

It is critical that a Family Office obtain a clear understanding that their fees are reasonable and that they obtain high quality, unconflicted services. Significant conflicts of interest are often overlooked or missed, not only at brokerage firms and private banks, but also among law firms, accounting firms, brokerage firms, and private banks.

Families face this predicament since they lead busy lives and their expertise often lies in running businesses outside the realm of institutional investing. Even when a family member does understand financial markets, the breadth and depth of challenges remain substantial. Too often, navigating institutional investing strategies distills down to over-reliance on a narrow set of trusted relationships, without properly assessing the performance of legal, tax, and accounting advisers that a family may utilize.

Family Office Services Provided

Manager Analysis can help families tap into skilled expertise that could help them ensure fair treatment, enhance their service levels, and reduce fees. Given our extensive experience assessing fee levels, commitment terms, portfolio construction, and overall quality of investment managers and service providers, we can address those factors that create the greatest vulnerabilities for families, while providing timely and thoughtful counsel to your family.

Performing a comprehensive review of your portfolios typically leads to enhanced communication with all service providers, stronger levels of support, potential material changes in investment managers (as needed) and improved and timely responsiveness to portfolio changes and market conditions.

Investment Portfolio Services Offered

Assessment of Key Service Providers (including asset managers, private banks, custodians and

multifamily offices)

Evaluation of Fees Paid (compared to market practices and value added)

Portfolio Analysis (with reconciliation to your family’s investment goals)

Assessment of Investment Strategies

Operational Due Diligence

Reviews of Partnership Agreements

Assessment of Investment Managers

Portfolio Management Services

Analysis of All Investments

Portfolio Construction Review

Manager Selection and Monitoring

Complex Real Estate Strategy Analysis

Risk Management

Liquidity Planning

Tax Analysis for Portfolio Holdings

Integration Services

Trust/Estate Documents Review

Disinterested Trustee Services

Financial Education of Family Members

Financial Planning and Budgeting

Expense Management

Contract Review

Staff Review and Career Development

Service Provider Coordination: Audit/Administration/Tax/Investments